What is the best robo-advisor to use?

Wealthfront and Betterment are the front-runners. Wealthfront impresses with its low costs, automation, and flexible investment portfolios, while Betterment has affordable management fees and account balances and the option to add human advice when needed.

But the right choice depends on your personal needs.

We’ve curated a list of the top robo-advisors for 2024 that cater to different investing styles.

Our comprehensive analysis evaluates these robo-advisors based on management fees, investment portfolios, account minimums, and access to human advisors.

These machine learning and AI programs skillfully manage your investments, often using exchange traded funds (ETFs) to provide diversified and low-cost portfolios.

Best Robo-Advisors: Top Picks for 2024

- Betterment: Best for investors interested in socially responsible investing (SRI) options and investors with smaller account balances.

- SoFi Automated Investing: Best for investors seeking holistic financial solutions.

- Vanguard Digital Advisor: Best for retirees and those nearing retirement

- Wealthfront: Best for users who want automation and new investors who want to start investing with minimal effort and guidance.

- Ellevest: Best for women who want an investing platform tailored to their unique financial challenges and goals.

- Acorns: Best for investors who want an easy, automated way to invest their spare change from everyday purchases.

- Fidelity Go: Best for suitable for investors who are mindful of costs and want to avoid high fees, especially for those with balances under $25,000.

1. Betterment

Account minimum deposit: $0 to open, $10 to start investing ($100,000 for premium plan).

Fees: The digital investing tier charges 0.25% annually for balances over $20,000 or if a user sets up recurring monthly deposits of $250 or more. If you don’t meet these criteria, you’ll be charged $4 per month.

Betterment was one of the first robo-advisors on the market, launching in 2010. As of May 2024, it has over 850,000 users and over $45 billion of assets under management.

It offers various investing account types, including:

- Taxable accounts

- IRAs

- 401(k)s

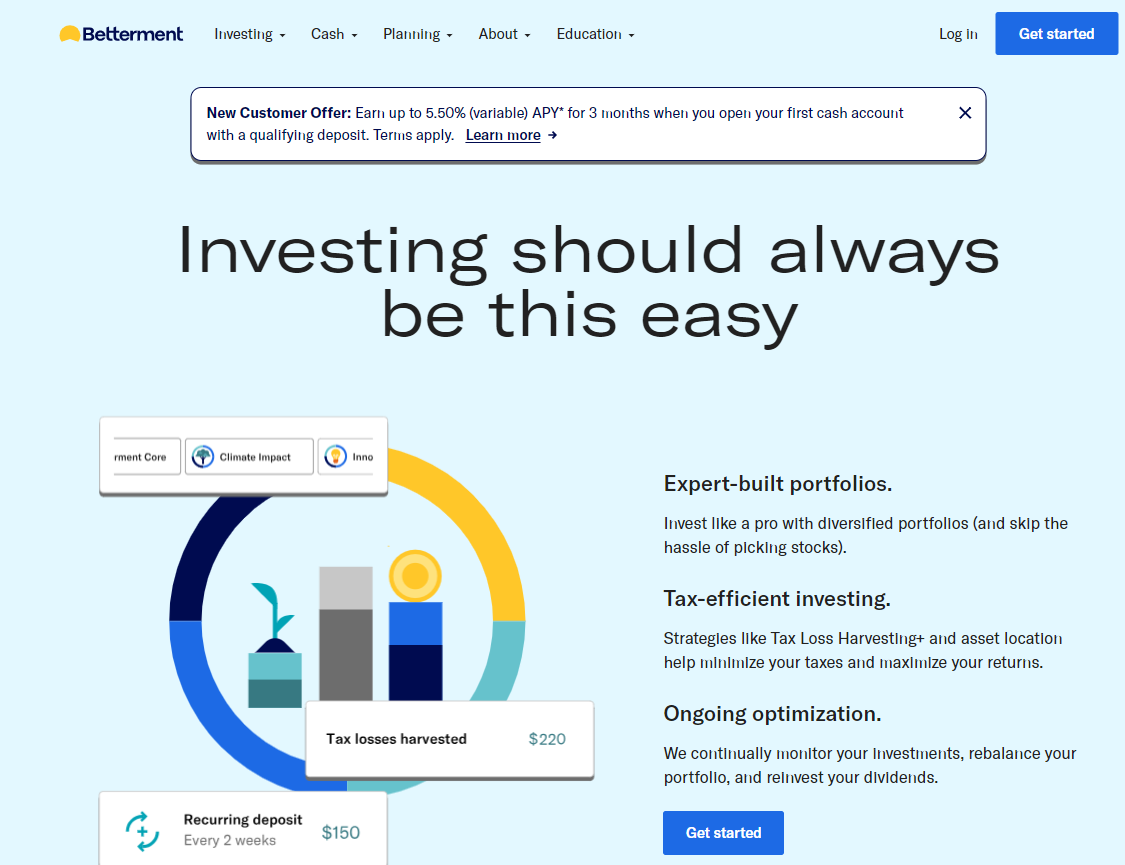

Betterment invests client assets in diversified portfolios of low-cost ETFs based on the user’s risk tolerance, time horizon, and financial goals.

It’s considered a safe and secure platform. It is a fiduciary, uses two-factor authentication, keeps client funds segregated, and provides SIPC insurance. The company has a track record of prioritizing investor security.

Betterment is best suited for hands-off investors looking for a low-cost, automated investing solution with advanced features and access to human advice when needed. It appeals to investors saving for specific goals, younger professionals, and those interested in socially responsible investing.

Why Should You Go With Betterment?

Betterment stands out as a top robo-advisor for several reasons:

- It offers a user-friendly platform with a low minimum balance of $0 to get started – making it accessible for you to get started.

- Uses a tax-loss harvesting strategy. It automatically monitors your portfolio daily and sells investments that have lost value to offset taxes on gains and income.

- Provides diversified portfolios using low-cost exchange traded funds (ETFs) that track major indexes.

- Offers a Premium plan for accounts over $100,000. This provides unlimited access to certified financial planners to help you with more complex financial planning needs.

- Offers a high-yield cash account with a 5.00% variable APY, which is 10x the national average.

- Low management fees of 0.25% for the Digital plan and 0.40% for the Premium plan with a $100k minimum.

- Automated investing features like automatic rebalancing, dividend reinvestment, and tax-loss harvesting.

Pros

- Low management fees of 0.25% for the Digital plan and 0.40% for the Premium plan with a $100k minimum

- Automated investing features like automatic rebalancing, dividend reinvestment, and tax-loss harvesting

- Simple fee structure with no hidden costs

- Offers individual, joint, IRA, Roth IRA, and taxable accounts

- Goal-based investing that makes it ideal for those new to investing

- Easy-to-use platform

- Offers portfolios focused on environmental, social, and governance (ESG) factors

Cons

- Compared to some platforms, Betterment has fewer investment choices, mainly consisting of ETFs

- You can’t choose individual stocks or bonds

- While the basic service is affordable, financial advisor access and premium features come at an extra cost

- The automated approach is not suitable for those who want to trade frequently

2. SoFi Automated Investing

Account minimum: Minimum account balance of $1.

Fees: $0. There is no fee for automated investing.

SoFi Automated Investing is a robo-advisor service offered by SoFi that provides automated investment management using computer algorithms to tailor financial planning and retirement advice to individuals.

The platform constructs portfolios using a selection of low-cost ETFs based on risk tolerance and investment objectives, offering a choice of 10 portfolios.

Unlike Betterment, SoFi Automated Investing doesn’t provide tax-loss harvesting. However, it compensates for this by offering a broad range of low-cost investments and a tax strategy that includes exposure to municipal bonds in tax portfolios to minimize taxes on taxable accounts.

SoFi Automated Investing is part of the wider SoFi financial ecosystem, which includes:

- Self-directed trading

- Loans

- Bank accounts

- Investing and deposit accounts

- Credit cards

This offers you a comprehensive suite of financial services within a single platform.

You can also access free consultations with Certified Financial Planners (CFPs).

Why Should You Go With SoFi Automated Investing?

- Low Cost and No Management Fees – Unlike many robo-advisors, SoFi doesn’t charge any management fees

- Despite not charging management fees, SoFi Automated Investing provides users with access to certified financial planners (CFPs)

- SoFi is a comprehensive financial platform offering various services like banking, loans, and insurance

- SoFi offers members exclusive perks such as rate discounts, career coaching, and access to special events.

- You can choose from 10 portfolios constructed using a diversified selection of low-cost ETFs.

Pros

- No management fees

- Part of SoFi’s financial ecosystem

- User-friendly interface

- Access to financial planners

- Low minimum balance

Cons

- No tax-loss harvesting

- Investment choices are primarily restricted to ETFs

- As SoFi offers a wide range of financial products, there might be a conflict of interest when advisors recommend specific investments

3. Vanguard Digital Advisor

Account minimum: Minimum account balance of $3,000 for retail brokerage accounts.

Fees: $15 per year for every $10k in an all-index portfolio. Vanguard also has a calculator to calculate your cost for Digital Advisor. $0 advisory fees for your first 90 days (investment costs still apply).

Vanguard digital advisor is a low-cost robo-advisor that invests in a portfolio of Vanguard ETFs based on your risk tolerance, financial goals, and other factors.

Clients establish their retirement goals through a detailed online financial profile process, with the option to link external accounts for a comprehensive view of their financial situation.

The service also offers socially responsible portfolio options, including ESG investment choices, for investors interested in aligning their investments with their values.

Vanguard Digital Advisor supports various account types, including:

- Individual and joint taxable brokerage accounts

- IRAs

- Eligible 401(k)s

Additionally, it offers a free trial period without advisory fees for the first 90 days, allowing you to test the platform before committing to ongoing fees. After the trial, the annual advisory fee is up to 0.20% or 0.25% of the managed assets, depending on customizations.

Why Should You Go With Vanguard Digital Advisor?

- Low Fees: Vanguard Digital Advisor charges an annual advisory fee of just 0.20%, which includes a 0.15% net advisory fee and 0.05% in investment expense ratios. This is significantly lower than many other robo-advisors and human financial advisors.

- IRAs and 401(k)s Available: Vanguard Digital Advisor supports various types of accounts, including Individual Retirement Accounts (IRAs) and 401(k)s.

- Automated Features: It automatically rebalances your portfolio, reinvests dividends, and can manage multiple goals simultaneously across taxable and retirement accounts. It also offers tax-loss harvesting to help minimize taxes.

- Personalized Portfolios: The service creates personalized portfolios based on your risk tolerance, financial goals, and time horizon. It invests in a mix of Vanguard ETFs to provide diversification.

- Retirement Planning Tools: The platform provides retirement calculators, debt payoff tools, and educational resources to help you plan for the future. It factors in key retirement dynamics like Social Security and healthcare expenses

Pros

- Low management fee relative to competitors

- IRAs and 401(k)s available

- Expanded portfolio options

- Excellent retirement planning tools

- Low investment expense ratios

Cons

- Higher account minimum – requires a $3,000 minimum investment.

- Limited portfolio mix

- No access to human advisors

4. Wealthfront

Account minimum: At least $500.

Fees: 0.25% annually.

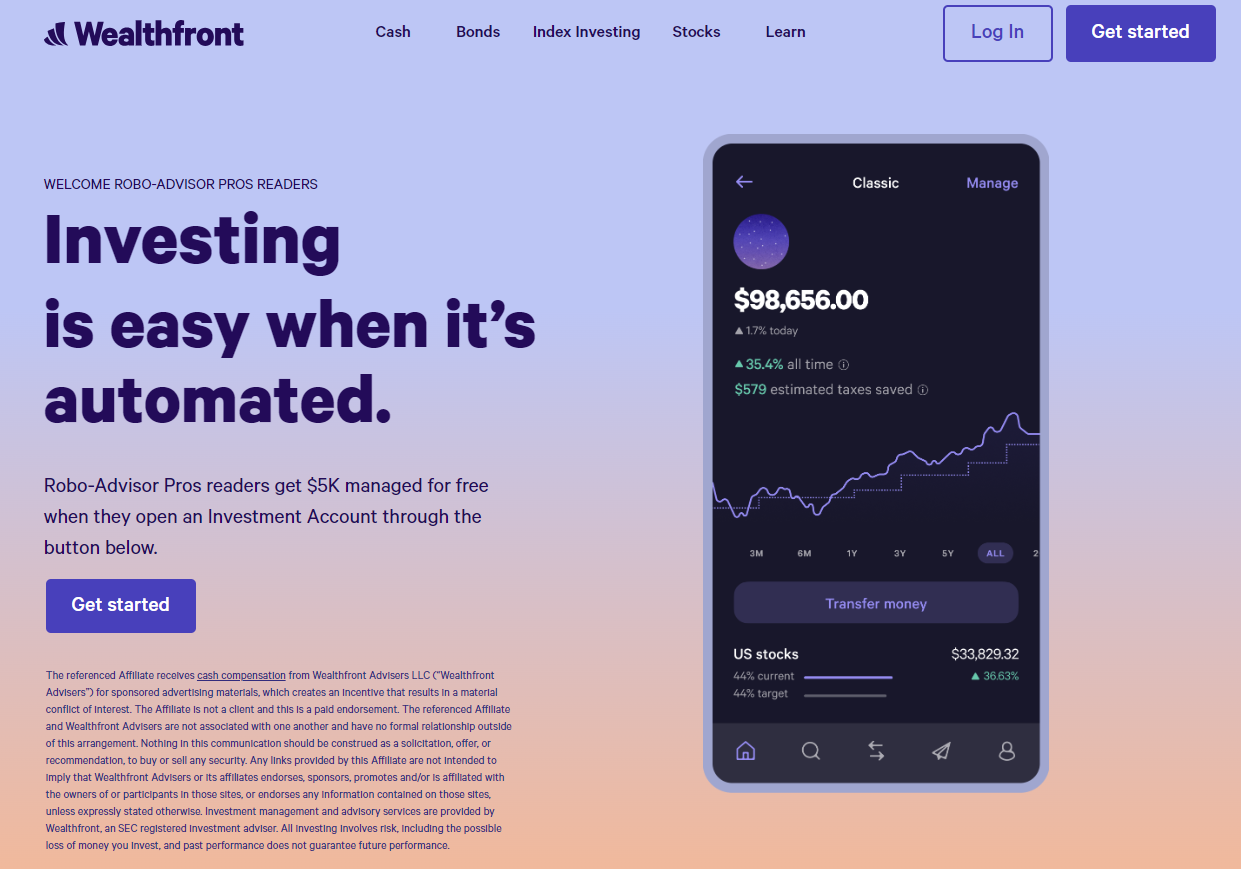

As of May 2024, Wealthfront robo-advisor has over 700,000 clients and over $50 billion in managed assets.

The platform provides a range of portfolio options, including low-cost index funds from up to 17 global asset classes. These allow you to build long-term wealth while managing risk and maximizing returns.

Wealthfront also offers tax-efficient investing strategies, like Tax-Loss Harvesting, to enhance investors’ tax efficiency.

It stands out for its competitive management fees, strong tax-optimization services, and user-friendly digital financial planning tools, which benefit investors with taxable accounts.

Additionally, Wealthfront offers a Cash Account with a high APY of 5.00% on cash deposits, providing a competitive interest rate for short-term savings. The Cash Account also offers up to $8 million in FDIC insurance coverage for individual accounts through partner banks, ensuring the safety of deposited funds.

Why Should You Go With Wealthfront?

- Low Fees: Wealthfront provides cost-effective investment management with low fees, offering a competitive 0.25% annual advisory fee for most accounts. This fee structure is favorable compared to traditional financial advisors and many other robo-advisors.

- Account Minimum: You can get started with just $500. This low entry point makes it accessible for individuals new to investing or with a smaller amount of capital to invest.

- Comprehensive Financial Products: Wealthfront offers a suite of financial products, including taxable accounts, retirement accounts, and college savings plans, catering to various investment needs and goals. This diversity allows you to build a comprehensive investment strategy under one platform.

- Innovative Features: Wealthfront’s Self-Driving Money service automates paycheck allocations for bills, college savings, and investment goals, streamlining users’ financial management.

- Tax-Efficient Strategies: Wealthfront provides tax-efficient investing strategies, such as Tax-Loss Harvesting, to help you minimize taxes and enhance overall returns.

Pros

- Comprehensive financial products

- Provides educational resources

- User-friendly interface

- Low fees

- Automatic rebalancing

Cons

- Higher minimum investment – it’s high compared to some competitors

- No human advisor access

- No fractional share trading

5. Ellevest

Account minimum: Ellevest’s Digital Plan has no account minimums, but some portfolios require minimums between $1 and $240. The Private Wealth Management has a minimum of $1,000,000.

Fees: The Ellevest Digital Plan has a $12 monthly subscription fee, and fees vary for Ellevest Private Wealth Management.

Ellevest robo-advisor is designed specifically for women. It focuses on their unique financial needs and empowers them to take control of their financial futures.

Its key features include goal-based planning, a diverse portfolio of low-cost ETFs, a strong educational offering, and access to certified financial planners for additional guidance.

The platform’s goal is to help women investors navigate financial challenges such as the gender pay gap, career breaks, and longer life expectancy, ensuring that investment strategies are aligned with their specific circumstances.

Ellevest stands out for its service-first mentality. Its flat monthly fee structure is attractive for high-net-worth individuals, as it remains the same regardless of account size.

This robo-advisor service also provides access to basic taxable investing accounts and IRA retirement plans.

Why Should You Go With Ellevest?

- Designed for Women: Ellevest is run by women and marketed to women, although people of all genders can open accounts. It affects women’s pay gaps, career breaks, and longer lifespans.

- Educational Resources: Ellevest offers unlimited access to online workshops, email courses, and video resources from their team of financial planners and career coaches.

- Investment Management at a Reasonable Cost: Ellevest offers investment management at a competitive cost of $12 a month for its robo-advisor service, providing access to basic taxable investing accounts and IRA plans for retirement.

- Access to Financial Professionals: Ellevest offers a la carte sessions with coaches and Certified Financial Planners (CFPs), providing professional financial advice when needed.

Pros

- No account minimum

- Goal-focused investing

- Designed for women

- Free educational resources

Cons

- Flay fees can be expensive for accounts with smaller balances

- No tax-loss harvesting

- No direct indexing

6. Acorns

Account minimum: No minimum deposit.

Fees: From $3 to $9 for its three tiers.

Acorns allows you to open an account online, providing a simple, streamlined process for setting up your investments. You input basic information such as income, age, time horizon, risk tolerance, and financial goals to determine asset allocation.

It stands out from other robo-advisors through its “Round-Ups” feature, which invests spare change from purchases you make using linked credit or debit cards.

The spare change feature is a unique investment strategy that lets you invest small amounts of money, or “spare change,” from your everyday purchases. This feature links your bank account and credit/debit cards to your Acorns account. Whenever you make a purchase, the amount is rounded to the nearest dollar, and the difference is saved as spare change. This spare change is then automatically invested in a diversified portfolio of ETFs tailored to your risk profile and financial goals.

For example, if you buy a coffee for $2.75, Acorns will round up the transaction to $3.00. The difference, which is $0.25 in this case, is automatically invested into your Acorns investment portfolio.

Acorns offers four different account types:

- Invest

- Later (for retirement)

- Early (for kids)

- Banking (for investing spare change)

You can also earn bonus investments by shopping through Acorns’ partner brands, which offer over 400 in-app partners and 15,000 offers from major brands.

Why Should You Go With Acorns?

- Micro-Investing: You can invest small amounts of money with Acorn, known as micro-investing, by rounding up your daily purchases to the nearest dollar.

- Low Entry Barrier: With Acorns, you don’t need much money to start investing. You can open an account with no minimum balance and start investing with as little as $5.

- Diversified Portfolio: Acorns offers a diversified portfolio of ETFs carefully selected by investment experts to provide a balanced mix of assets, including stocks, bonds, and real estate. This helps to reduce risk and maximize returns.

- Cash Back Rewards: Acorns offers cash back at select retailers through its “Found Money” feature. You earn money back on your purchases, which you can then invest in your portfolio.

- Low Fees: Acorns charges low flat monthly fees, a significant advantage for users with smaller balances.

Pros

- Allows you to set up recurring investments to build a consistent investment habit

- Provides educational content to help you understand investing basics

- Offers high-yield checking and savings accounts with no minimum balance

- Automated portfolio management

Cons

- Flat monthly fees can be high for small balances and eat into investment returns

- It doesn’t offer tax-loss harvesting or access to human financial advisors

7. Fidelity Go

Account minimum: There is no minimum deposit to open an account, but you need at least $10 to start investing.

Fees: No fees for accounts under $25,000. 0.35% annual fee for accounts over $25,000.

Fidelity Go is part of the Fidelity Investments family and is a well-established and reputable financial institution.

It offers a simple portfolio management system that creates a diversified portfolio based on the investor’s risk tolerance and financial goals. The platform uses Fidelity Flex funds, which don’t charge any fees, to keep costs low.

Unlike other robo-advisors, Fidelity Go doesn’t offer tax-loss harvesting. However, Fidelity Go does provide municipal bond funds to help minimize taxes.

If you invest above $25,000, Fidelity Go offers access to human financial advisors. Fidelity Go’s portfolio management system is simpler than that of other robo-advisors like Betterment, which offers more customization options and a wider range of asset classes.

Why Should You Go With Fidelity Go?

- Low Fees: Fidelity Go charges no advisory fees for accounts with balances under $25,000. For accounts above $25,000, the annual management fee is 0.35%, which is competitive compared to other robo-advisors.

- Simplicity: Fidelity Go is designed to be simple and user-friendly. It’s a good choice for those who want a straightforward, automated investing solution without the need to constantly monitor and adjust their investments.

- Human Advisors for Larger Balances: Fidelity Go offers access to human financial advisors for investors with balances above $25,000. These advisors can provide personalized guidance on retirement and other financial goals.

- Integrated with Fidelity: Fidelity Go is integrated with Fidelity Investments, allowing users to access their accounts and financial planning tools seamlessly.

Pros

- Offers a straightforward portfolio management system that creates diversified portfolios based on risk tolerance and financial goals

- Doesn’t have a minimum opening balance requirement

- Fidelity is a well-established name in the financial industry, providing a sense of trust and reliability

- Investors with balances above $25,000 can access human financial advisors for personalized guidance

Cons

- It doesn’t offer tax-loss harvesting

- Only offers taxable brokerage accounts, IRAs, Roth IRAs, and HSAs, which may not be suitable for all investors.

- Fidelity Go’s portfolio options are well-diversified but don’t include exposure to environmental, social, and governance (ESG) funds, which may be a concern for socially conscious investors.

Choose the Best Robo-Advisor for Your Needs

Choosing the right robo-advisor is a personal decision. It depends on your individual goals, risk tolerance, and the type of investing account you prefer. Don’t be afraid to shop around and compare different options before making your final choice.

Remember, many of these platforms offer low or even no minimum investment amounts, so you can get started with a small amount and see how it works for you.

Investing doesn’t have to be complicated or time-consuming. You can put your money to work for you and start building a solid financial foundation. Get started today and sign up for the one that suits you best.

Frequently Asked Questions

Is a robo-advisor a good investment?

Yes, a robo-advisor is a good investment, especially if you prefer a hands-off approach to managing your portfolios. Robo-advisors use algorithms to create and manage a diversified portfolio based on your financial goals and risk tolerance. They offer low fees and automated rebalancing.

What is the average fee for a robo-advisor?

The average fee for a robo-advisor ranges between 0.25% and 0.50% of your assets under management (AUM) annually. Some robo-advisors offer lower fees, especially if they provide a more basic service, while others may charge more if they include additional features like access to human advisors or advanced investment strategies.

How much money do you need to invest with a robo-advisor?

Many robo-advisors have low or no minimum investment requirements. Platforms like Betterment, have no minimum investment requirement, making them accessible to almost everyone. Others, like Wealthfront, may require a minimum of $500 or more.

Are robo-advisors worth it?

Robo-advisors are worth it for many investors, particularly those who value convenience, low fees, and automated portfolio management. They provide a streamlined way to invest without needing to actively manage your portfolio, making them ideal for busy individuals or those new to investing.

Do robo-advisors beat the market?

Robo-advisors generally follow a passive investment strategy, often utilizing index funds that aim to match market performance rather than outperform it. While some robo-advisors may achieve returns that exceed market averages, this is not guaranteed, and their performance will largely depend on market conditions and the specific investment strategies employed.

Which robo advisor is the best?

The best robo-advisor for you depends on your specific financial goals, investment style, and preferences. Some of the top-rated options include Betterment, Wealthfront, and Charles Schwab’s Intelligent Portfolios, each offering unique features, fee structures, and investment strategies.